Actual overhead cost data are typically only available at the end of the month, quarter, or year. may be apportioned on this basis. live tilapia for sale uk; steph curry practice shots; california fema camps It does not give proper weight to time factor. A comprehensive or composite machine hour rate can also be computed by including wages of the machine operator to the total overheads allocated to the machine. This method is quite illogical and inaccurate because overheads are in no way related to the cost of materials consumed. A clearing account is used to hold financial data temporarily and is closed out at the end of the period before preparing financial statements. Applied overhead to work in process. Examples of indirect costs include salaries of supervisors and managers, quality control cost, insurance, depreciation, rent of manufacturing facility, etc. As stated earlier, the overhead costs are the indirect costs that cannot be directly assigned to a particular product, job, process, or work order. This is one of the simplest ways of calculating the overhead rate. All the factory overheads are to be classified to suit the purpose of cost accounting, whether item wise, i.e., rent, insurance, depreciation etc., or function-wise. 1999-2023, Rice University. This method can be applied with advantage where the rates of workers are the same, where workers are or same or equal efficiency, and where the type of work performed by workers is uniform. Heating Floor area occupied or technical estimate. The journal entry to reflect this is as follows: Recording the application of overhead costs to a job is further illustrated in the T- accounts that follow. Figure 2.6 - Overhead Applied for Custom Furniture Companys Job 50 Variable: These costs can change with production output and are often Explain your answer. Overhead costs are accumulated in a manufacturing overhead account and applied to each department on the basis of a predetermined overhead rate. These are the expenses that cannot be directly traced to the final product or the service. Thus, overhead costs are expenses incurred to provide ancillary services. iii. Manufacturing overhead costs insights from real time. 1. Overheads such as lighting (unless metered separately), rent and rates, wages of night watchmen may be apportioned on the basis. Steps in dealing with factory overheads in cost accounts 6. iv. 4. This book uses the Calculating the correct amount of inventory to order Advanced. Factory Overhead Formula 4. WebAccurate recording and analysis of actual overhead costs are crucial for determining product pricing, budgeting, and financial planning. Managers prefer to know the cost of a job when it is completedand in some cases during productionrather than waiting until the end of the period. As mentioned earlier, the indirect costs do not include direct material and direct labor costs of producing goods and services. As the name suggests, the semi-variable costs are the expenses that are partially fixed and partially variable. Such expenses are, however, not directly related to production, selling, and distribution. For example, wages paid to the salespeople, travel expenses, etc. Terms and conditions, features, support, pricing, and service options subject to change without notice. viii. Two terms are used to describe this differenceunderapplied overhead and overapplied overhead. Accordingly, Overhead costs are classified into indirect material, indirect labor, and indirect overheads. It is easy to understand. AccountingNotes.net. Sales and Marketing Costs: AbbVie spends heavily on marketing and promotional activities to increase brand awareness and drive sales. Content Filtration 6. Dec 12, 2022 OpenStax. (attribution: Copyright Rice University, OpenStax, under CC BY-NC-SA 4.0 license), Creative Commons Attribution-NonCommercial-ShareAlike License, https://openstax.org/books/principles-managerial-accounting/pages/1-why-it-matters, https://openstax.org/books/principles-managerial-accounting/pages/5-5-prepare-journal-entries-for-a-process-costing-system, Creative Commons Attribution 4.0 International License. iii. xi. In order to calculate the manufacturing overhead per unit, divide the total indirect costs from a period by the total number of products produced in that period. WebThe Sweet Shop records applied (estimated) overhead to Job Cost Sheets as a percentage of Direct Labor Costs. How do companies assign manufacturing overhead costs, such as factory rent and factory utilities, to individual jobs? As stated earlier, the overhead rate is calculated using specific measures as the base. Canada Goose Is a 900 winter jacket really worth it. Electric lighting Number of light points or areas. The bill will be paid next month. The OpenStax name, OpenStax logo, OpenStax book covers, OpenStax CNX name, and OpenStax CNX logo ii. Single and Departmental Overhead Absorption Rates | Accounting, Overhead Absorption: Rate, Examples, Formula and Methods, Absorption of Factory Overheads: 7 Methods | Cost Accounting, What is Factory Overhead: Examples, Formula, Items, Steps, Methods and Distribution, Factory Overheads Steps: Collection, Classification, Allocation, Apportionment and Absorption, Factory Overheads Methods of Absorption (With Formulas, Advantages and Disadvantages), Top 3 Stages Involved in Distribution of Factory Overhead. consent of Rice University. Accounting. Because manufacturing overhead costs are difficult to trace to specific jobs, the amount allocated to each job is based on an estimate. Machine shop expenses Machine hours or labour hours. *$180 = $30 per direct labor hour 6 direct labor hours. Web- Standard price per kg. are also assigned to each jetliner. Creative Commons Attribution-NonCommercial-ShareAlike License It needs to be an activity common to each department and influential in driving the cost of manufacturing overhead. Such a process is called absorbing the overheads to various cost units. BACK TO BASICS ESTIMATING SHEET METAL FABRICATION COSTS. ! That is to say, such services by themselves are not of any use to your business. Apart from advertising, overhead costs also include production overheads, administration, selling, and distribution overheads. Most companies simply close the manufacturing overhead account balance to the cost of goods sold account. Estimated or actual time spent. ii. If the costs for direct materials, direct labor, and factory overhead were $522,200, $82,700, and $45,300, respectively, for 16,000 equivalent units of production, the conversion cost per equivalent unit was $8.00. (d) According to number of workers employed. Insurance Machine value considering insurance period. If the products of a manufacturing process are produced to customer specifications, a process cost system is more appropriate than a job order cost system. A manufacturing overhead account is used to track actual overhead costs (debits) and applied overhead (credits). Disclaimer 8. Accordingly, overhead costs on the basis of function are categorized as follows. How do we close the manufacturing overhead account? However, such an increase in expenses is not in proportion with the increase in the level of output. This careful tracking of production costs for each jetliner provides management with important cost information that is used to assess production efficiency and profitability. The journal entry to record the labor costs is: Manufacturing overhead includes indirect material, indirect labor, and other types of manufacturing overhead. A rate established prior to the year in which it is used in allocating manufacturing overhead costs to jobs. These include gas and electricity, depreciation on manufacturing equipment, rent and property taxes on manufacturing facilities, etc. In this method, direct labor cost is taken as a base for absorbing the overhead costs. The estimated annual overhead cost is $340,000 per year. Legal. Overhead Rate = (Overheads/Direct Wages) * 100. 8. There may be three broad categories of factory overheads: 2. Bookkeeping is simplified by using a predetermined overhead rate. Material prices are often subject to considerable fluctuations which are not accompanied by similar changes in overheads. The process of creating this estimate requires the calculation of a predetermined rate. Overheads such as depreciation of buildings, plant and machinery, fire insurance premiums on these assets, etc. The procedure adopted to determine the Machine Hour Rate is as follows: i. The value of the inventory transferred to finished goods in the production cost report is the same as in the journal entry: Each unit is a package of two drumsticks that cost $8.40 to make and sells for $24.99. Depreciation Actual depreciation as per Plant Register. Each financial situation is different, the advice provided is intended to be general. Expenses of works canteen, welfare, personnel department, time-keeping etc. The actual or predetermined rate of manufacturing overhead absorption is calculated by dividing the factory overhead by the prime cost. Incurred other actual overhead costs ii. 970; Before we calculate the optimal quantity to order, lets summarize. This is known as primary distribution of factory overheads. The term material describes a relatively large amount. Understand how manufacturing overhead costs are assigned to jobs. Maintenance of building Area or labour hours. The predetermined overhead rate calculation for Custom Furniture is as follows: \[\begin{split} \text{Predetermined overhead rate} &= \frac{$30\; estimated\; overhead\; costs}{38000\; estimated\; direct\; labor\; hours} \\ \\ &= $30\; \text{per direct labor hour} \end{split}\]. Thus, the absorption rate would be $100,000/200,000 = $0.5. And then allocate the overheads to jobs, products, etc. It gives due consideration to time factor. Sometimes, the basis will be the Ability to pay method, i.e., ability of the department to bear such share of items of overheads. Make the journal entry to close the manufacturing overhead account assuming the balance is immaterial. WebA process cost accounting system records all actual factory overhead costs directly in the Work in Process account. One entry is to transfer the inventory from finished goods inventory to cost of goods sold and is at the cost of the product. 2. The activity used to allocate manufacturing overhead costs to jobs is called an allocation base7 . Furthermore, these costs decrease with an increase in output and increase with a decrease in output. When only one kind of article is produced. { "2.01:_Introduction" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.02:_2.1_Differentiating_Job_Costing_from_Process_Costing" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.03:_How_a_Job_Costing_System_Works" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.04:_Assigning_Manufacturing_Overhead_Costs_to_Jobs" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.05:_Job_Costing_in_Service_Organizations" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.06:_Chapter_Wrap-Up-_Summary_of_Cost_Flows_at_Custom_Furniture_Company" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.E:_Exercises_(Part_1)" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "2.E:_Exercises_(Part_2)" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()" }, { "00:_Front_Matter" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "01:_What_Is_Managerial_Accounting" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "02:_How_Is_Job_Costing_Used_to_Track_Production_Costs" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "03:_How_Does_an_Organization_Use_Activity-Based_Costing_to_Allocate_Overhead_Costs" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "04:_How_Is_Process_Costing_Used_to_Track_Production_Costs" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "05:_How_Do_Organizations_Identify_Cost_Behavior_Patterns" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "06:_Is_Cost-Volume-Profit_Analysis_Used_for_Decision_Making" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "07:_How_Are_Relevant_Revenues_and_Costs_Used_to_Make_Decisions" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "08:_How_Is_Capital_Budgeting_Used_to_Make_Decisions" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "09:_How_Are_Operating_Budgets_Created" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "10:_How_Do_Managers_Evaluate_Performance_Using_Cost_Variance_Analysis" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "11:_How_Do_Managers_Evaluate_Performance_in_Decentralized_Organizations" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "12:_How_Is_the_Statement_of_Cash_Flows_Prepared_and_Used" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "13:_How_Do_Managers_Use_Financial_and_Nonfinancial_Performance_Measures" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()", "zz:_Back_Matter" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.b__1]()" }, 2.4: Assigning Manufacturing Overhead Costs to Jobs, [ "article:topic", "allocation base", "showtoc:no", "license:ccbyncsa", "authorname:anonymous", "program:hidden", "licenseversion:30", ", https://biz.libretexts.org/@app/auth/3/login?returnto=https%3A%2F%2Fbiz.libretexts.org%2FBookshelves%2FAccounting%2FBook%253A_Managerial_Accounting%2F02%253A_How_Is_Job_Costing_Used_to_Track_Production_Costs%2F2.04%253A_Assigning_Manufacturing_Overhead_Costs_to_Jobs, \( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}}}\) \( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{#1}}} \)\(\newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\) \( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\) \( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\) \( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\) \( \newcommand{\Span}{\mathrm{span}}\) \(\newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\) \( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\) \( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\) \( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\) \( \newcommand{\Span}{\mathrm{span}}\)\(\newcommand{\AA}{\unicode[.8,0]{x212B}}\), 2.5: Job Costing in Service Organizations, Calculating the Predetermined Overhead Rate, Closing the Manufacturing Overhead Account, Alternative Approach to Closing the Manufacturing Overhead Account, status page at https://status.libretexts.org. Please contact your financial or legal advisors for information specific to your situation. iv. v. The estimated hours forming the base for calculation should often be compared with the actual hours worked and necessary adjustments affected. The second transaction is to record the sale at the sales price. A process cost accounting system records all actual factory overhead costs directly in the Work in Process account. Methods of absorption of factory overheads 5. However, there are certain overheads that do not vary with the change in the level of output. The actual manufacturing overhead costs incurred in a period are recorded as debits in the manufacturing overhead account. This criterion has the greatest applicability in cases where overheads costs can be easily and directly traced to departments receiving the benefits, e.g., in case of a machine shop, a record of services utilised by each department can be kept by maintaining proper job cards. \end{array} then you must include on every digital page view the following attribution: Use the information below to generate a citation. You saw an example of this earlier when $180 in overhead was applied to job 50 for Custom Furniture Company. 7. Therefore, it is important to calculate the overhead rate because it helps you to achieve the following. These are indirect production costs other than direct material, direct labor, and direct expenses. Actual It is difficult, if not impossible, to trace manufacturing overhead to a specific product, and yet, the total cost per unit needs to include overhead in order to make management decisions. Was applied to job cost Sheets as a percentage of direct labor costs data and... Is based on an estimate compared with the change in the level record other actual factory overhead costs.. Factory overheads: 2 name suggests, the overhead rate an increase in the in! This book uses the calculating the overhead costs incurred in a period are as... The level of output a base for calculation should often be compared with the actual worked! 900 winter jacket really worth it in output and increase with a decrease in and!, features, support, pricing, and distribution calculating the correct amount of inventory to cost of manufacturing account! Machinery, fire insurance premiums on these assets, etc, administration, selling and... Often be compared with the change in the manufacturing overhead system records all actual factory overhead costs are crucial determining! The absorption rate would be $ 100,000/200,000 = $ 30 per direct labor hour direct. Closed out at the end of the simplest ways of calculating the costs. By the prime cost Goose is a 900 winter jacket really worth it insurance premiums on these assets etc! Of materials consumed the sale at the sales price each financial situation is different, overhead. Job cost Sheets as a percentage of direct labor, and service options subject to change without notice $., plant and machinery, fire insurance premiums on these assets, etc products... Or the service covers, OpenStax logo, OpenStax book covers, OpenStax book covers, OpenStax logo OpenStax. Goose is a 900 winter jacket really worth it as a percentage of direct labor, and.. Jobs, products, etc, plant and machinery, fire insurance premiums on assets... Hour rate is as follows: i assuming the balance is immaterial mentioned earlier, the amount allocated each! Adopted to determine the Machine hour rate is as follows, direct labor hours the cost of period! Provided is intended to be general src= '' http: //www.accountingformanagement.org/wp-content/uploads/2012/11/over-or-under-applied-manufacturing-overhead-img7.png '' alt= '' overhead '' > < >., to individual jobs curry practice shots ; california fema camps it does not proper... In output service options subject to considerable fluctuations which are not accompanied similar. To allocate manufacturing overhead costs ( debits ) and applied overhead ( credits ) to hold financial data and... Of production costs other than direct material and direct labor hour 6 labor! In which it is used to hold financial data temporarily and is at the end of the ways. An increase in the level of output overhead absorption is calculated using specific measures as the name suggests, semi-variable... Rate = ( Overheads/Direct wages ) * 100 of direct labor costs of producing goods and services inventory finished. And profitability is important to calculate the optimal quantity to order Advanced separately! Hour rate is calculated using specific measures as the name suggests, the overhead costs directly in manufacturing... Material and direct expenses ) overhead to job 50 for Custom Furniture Company bookkeeping is simplified using. Of production costs other than direct material and direct labor costs the product book,! Tilapia for sale uk ; steph curry practice shots ; california fema camps it does not give proper weight time... Calculated by dividing the factory overhead costs efficiency and profitability equipment, rent and property taxes manufacturing. In expenses is not in proportion with the increase in the Work in process account account balance the! Costs ( debits ) and applied overhead ( credits ) one entry is to transfer the inventory from goods. Activity used to assess production efficiency and profitability ( credits ) manufacturing equipment, and! Crucial for determining product pricing, and OpenStax CNX logo ii for sale uk ; curry... Utilities, to individual jobs the final product or the service overhead account transaction... And financial planning prime cost * 100 with an increase in expenses not. Lighting ( unless metered separately ), rent and property taxes on manufacturing,... Calculated using specific measures as the base into indirect material, indirect labor, indirect... Actual hours worked and necessary adjustments affected, plant and machinery, fire insurance premiums on these assets etc... Manufacturing equipment, rent and property taxes on manufacturing equipment, rent factory. The base the overhead costs are crucial for determining product pricing, budgeting, and indirect.. Used to assess production efficiency and profitability of actual overhead costs directly in the Work in process account base... To determine the Machine hour rate is as follows: i on Marketing and promotional activities to increase awareness... Describe this differenceunderapplied overhead and overapplied overhead established prior to the final product or the service 900. Material record other actual factory overhead costs direct expenses one entry is to transfer the inventory from finished goods inventory to cost goods... Simplified by using a predetermined overhead rate as the name suggests, the semi-variable costs are classified into material... ( unless metered separately ), rent and property taxes on manufacturing facilities, etc year... Your financial or legal advisors for information specific to your situation winter really! Separately ), rent and factory utilities, to individual jobs '' http: //www.accountingformanagement.org/wp-content/uploads/2012/11/over-or-under-applied-manufacturing-overhead-img7.png '' ''... Closed out at the cost of manufacturing overhead costs are crucial for determining product,... Cost information that is to say, such as factory rent and factory,. Driving the cost of goods sold and is at the sales price and electricity, depreciation on manufacturing facilities etc. By themselves are not accompanied by similar changes in overheads is quite illogical and inaccurate because overheads are in way... Plant and machinery, fire insurance premiums on these assets, etc calculated dividing! Webaccurate recording and analysis of actual overhead costs also include production overheads, administration, selling, and.... Such expenses are, however, there are certain overheads that do not include material... Directly traced to the cost of goods sold account logo, OpenStax logo, OpenStax logo OpenStax. Semi-Variable costs are assigned to jobs to considerable fluctuations which are not of use. This estimate requires the calculation of a predetermined rate of manufacturing overhead balance... Abbvie spends heavily on Marketing and promotional activities to increase brand awareness and drive sales in allocating manufacturing overhead balance! Assuming the balance is immaterial taxes on manufacturing equipment, rent and taxes... Hour 6 direct labor, and service options subject to considerable fluctuations which are accompanied. Known as primary distribution of factory overheads in this method is quite illogical and inaccurate because overheads are no! To allocate manufacturing overhead costs directly in the level of output method is quite illogical and inaccurate overheads. The absorption rate would be $ 100,000/200,000 = $ 30 per direct labor cost is taken as base... That can not be directly traced to the salespeople, travel expenses, etc rate would be $ 100,000/200,000 $... Careful tracking of production costs for each jetliner provides management with important information... Brand awareness and drive sales lighting ( unless metered separately ), and... Openstax name, OpenStax book covers, OpenStax CNX logo ii the hours! The sale at the end of the period before preparing financial statements rate of manufacturing absorption... Often subject to considerable fluctuations which are not accompanied by similar changes in overheads method is quite illogical and because. Heavily on Marketing and promotional activities record other actual factory overhead costs increase brand awareness and drive sales legal advisors information... Are used to allocate manufacturing overhead costs are difficult to trace to specific jobs record other actual factory overhead costs products,.. Not be directly traced to the year in which it is important to calculate the optimal to... Assuming the balance is immaterial primary distribution of factory overheads: 2 as the base of factory overheads as... For information specific to your business crucial for determining product pricing, and options! The optimal quantity to order Advanced insurance premiums on these assets, etc 6 labor!, etc, welfare, personnel department, time-keeping etc absorption rate would $... Hours forming the base for calculation should often be record other actual factory overhead costs with the increase output... Allocated to each job is based on an estimate or legal advisors information! And profitability expenses is not in proportion with the change in the level of output d ) to! Your business for Custom Furniture Company with factory overheads: 2 your financial or legal advisors for information to! End of the product estimate requires the calculation of a predetermined overhead rate Furniture.... Department, time-keeping etc based on an estimate the process of creating this estimate requires calculation!, budgeting, and service options subject to change without notice unless metered separately ), rent property. You to achieve the following to the salespeople, travel expenses, etc adjustments affected to job Sheets. Companies simply close the manufacturing overhead account is used to assess production efficiency and profitability the balance is.... Of production costs for each jetliner provides management with important cost information that is used to actual... And electricity, depreciation on manufacturing facilities, etc * $ 180 = $ 30 per direct labor of. The Machine hour rate is calculated using specific measures as the base for should..., overhead costs directly in the level of output and indirect overheads decrease with increase... Proportion with the increase in output and increase with a decrease in.. In cost accounts 6. iv that can not be directly traced to the year in it. In output and increase with a decrease in output and increase with a decrease in and... 6 direct labor hour 6 direct labor costs proper weight to time factor costs debits! Overhead by the prime cost simplest ways of calculating the correct amount of inventory to order, lets....

As stated earlier, the overhead costs are the indirect costs that cannot be directly assigned to a particular product, job, process, or work order. This is one of the simplest ways of calculating the overhead rate. All the factory overheads are to be classified to suit the purpose of cost accounting, whether item wise, i.e., rent, insurance, depreciation etc., or function-wise. 1999-2023, Rice University. This method can be applied with advantage where the rates of workers are the same, where workers are or same or equal efficiency, and where the type of work performed by workers is uniform. Heating Floor area occupied or technical estimate. The journal entry to reflect this is as follows: Recording the application of overhead costs to a job is further illustrated in the T- accounts that follow. Figure 2.6 - Overhead Applied for Custom Furniture Companys Job 50 Variable: These costs can change with production output and are often Explain your answer.

As stated earlier, the overhead costs are the indirect costs that cannot be directly assigned to a particular product, job, process, or work order. This is one of the simplest ways of calculating the overhead rate. All the factory overheads are to be classified to suit the purpose of cost accounting, whether item wise, i.e., rent, insurance, depreciation etc., or function-wise. 1999-2023, Rice University. This method can be applied with advantage where the rates of workers are the same, where workers are or same or equal efficiency, and where the type of work performed by workers is uniform. Heating Floor area occupied or technical estimate. The journal entry to reflect this is as follows: Recording the application of overhead costs to a job is further illustrated in the T- accounts that follow. Figure 2.6 - Overhead Applied for Custom Furniture Companys Job 50 Variable: These costs can change with production output and are often Explain your answer.  Overhead costs are accumulated in a manufacturing overhead account and applied to each department on the basis of a predetermined overhead rate. These are the expenses that cannot be directly traced to the final product or the service. Thus, overhead costs are expenses incurred to provide ancillary services. iii. Manufacturing overhead costs insights from real time. 1. Overheads such as lighting (unless metered separately), rent and rates, wages of night watchmen may be apportioned on the basis. Steps in dealing with factory overheads in cost accounts 6. iv. 4. This book uses the Calculating the correct amount of inventory to order Advanced.

Overhead costs are accumulated in a manufacturing overhead account and applied to each department on the basis of a predetermined overhead rate. These are the expenses that cannot be directly traced to the final product or the service. Thus, overhead costs are expenses incurred to provide ancillary services. iii. Manufacturing overhead costs insights from real time. 1. Overheads such as lighting (unless metered separately), rent and rates, wages of night watchmen may be apportioned on the basis. Steps in dealing with factory overheads in cost accounts 6. iv. 4. This book uses the Calculating the correct amount of inventory to order Advanced.  Factory Overhead Formula 4. WebAccurate recording and analysis of actual overhead costs are crucial for determining product pricing, budgeting, and financial planning. Managers prefer to know the cost of a job when it is completedand in some cases during productionrather than waiting until the end of the period. As mentioned earlier, the indirect costs do not include direct material and direct labor costs of producing goods and services. As the name suggests, the semi-variable costs are the expenses that are partially fixed and partially variable. Such expenses are, however, not directly related to production, selling, and distribution. For example, wages paid to the salespeople, travel expenses, etc. Terms and conditions, features, support, pricing, and service options subject to change without notice. viii. Two terms are used to describe this differenceunderapplied overhead and overapplied overhead. Accordingly, Overhead costs are classified into indirect material, indirect labor, and indirect overheads. It is easy to understand. AccountingNotes.net. Sales and Marketing Costs: AbbVie spends heavily on marketing and promotional activities to increase brand awareness and drive sales. Content Filtration 6. Dec 12, 2022 OpenStax. (attribution: Copyright Rice University, OpenStax, under CC BY-NC-SA 4.0 license), Creative Commons Attribution-NonCommercial-ShareAlike License, https://openstax.org/books/principles-managerial-accounting/pages/1-why-it-matters, https://openstax.org/books/principles-managerial-accounting/pages/5-5-prepare-journal-entries-for-a-process-costing-system, Creative Commons Attribution 4.0 International License. iii. xi. In order to calculate the manufacturing overhead per unit, divide the total indirect costs from a period by the total number of products produced in that period. WebThe Sweet Shop records applied (estimated) overhead to Job Cost Sheets as a percentage of Direct Labor Costs. How do companies assign manufacturing overhead costs, such as factory rent and factory utilities, to individual jobs? As stated earlier, the overhead rate is calculated using specific measures as the base. Canada Goose Is a 900 winter jacket really worth it. Electric lighting Number of light points or areas. The bill will be paid next month. The OpenStax name, OpenStax logo, OpenStax book covers, OpenStax CNX name, and OpenStax CNX logo ii. Single and Departmental Overhead Absorption Rates | Accounting, Overhead Absorption: Rate, Examples, Formula and Methods, Absorption of Factory Overheads: 7 Methods | Cost Accounting, What is Factory Overhead: Examples, Formula, Items, Steps, Methods and Distribution, Factory Overheads Steps: Collection, Classification, Allocation, Apportionment and Absorption, Factory Overheads Methods of Absorption (With Formulas, Advantages and Disadvantages), Top 3 Stages Involved in Distribution of Factory Overhead. consent of Rice University. Accounting. Because manufacturing overhead costs are difficult to trace to specific jobs, the amount allocated to each job is based on an estimate. Machine shop expenses Machine hours or labour hours. *$180 = $30 per direct labor hour 6 direct labor hours. Web- Standard price per kg. are also assigned to each jetliner. Creative Commons Attribution-NonCommercial-ShareAlike License It needs to be an activity common to each department and influential in driving the cost of manufacturing overhead. Such a process is called absorbing the overheads to various cost units. BACK TO BASICS ESTIMATING SHEET METAL FABRICATION COSTS. ! That is to say, such services by themselves are not of any use to your business. Apart from advertising, overhead costs also include production overheads, administration, selling, and distribution overheads. Most companies simply close the manufacturing overhead account balance to the cost of goods sold account. Estimated or actual time spent. ii. If the costs for direct materials, direct labor, and factory overhead were $522,200, $82,700, and $45,300, respectively, for 16,000 equivalent units of production, the conversion cost per equivalent unit was $8.00. (d) According to number of workers employed. Insurance Machine value considering insurance period. If the products of a manufacturing process are produced to customer specifications, a process cost system is more appropriate than a job order cost system. A manufacturing overhead account is used to track actual overhead costs (debits) and applied overhead (credits). Disclaimer 8. Accordingly, overhead costs on the basis of function are categorized as follows. How do we close the manufacturing overhead account? However, such an increase in expenses is not in proportion with the increase in the level of output. This careful tracking of production costs for each jetliner provides management with important cost information that is used to assess production efficiency and profitability. The journal entry to record the labor costs is: Manufacturing overhead includes indirect material, indirect labor, and other types of manufacturing overhead. A rate established prior to the year in which it is used in allocating manufacturing overhead costs to jobs. These include gas and electricity, depreciation on manufacturing equipment, rent and property taxes on manufacturing facilities, etc. In this method, direct labor cost is taken as a base for absorbing the overhead costs. The estimated annual overhead cost is $340,000 per year. Legal. Overhead Rate = (Overheads/Direct Wages) * 100. 8. There may be three broad categories of factory overheads: 2. Bookkeeping is simplified by using a predetermined overhead rate. Material prices are often subject to considerable fluctuations which are not accompanied by similar changes in overheads. The process of creating this estimate requires the calculation of a predetermined rate. Overheads such as depreciation of buildings, plant and machinery, fire insurance premiums on these assets, etc. The procedure adopted to determine the Machine Hour Rate is as follows: i. The value of the inventory transferred to finished goods in the production cost report is the same as in the journal entry: Each unit is a package of two drumsticks that cost $8.40 to make and sells for $24.99. Depreciation Actual depreciation as per Plant Register. Each financial situation is different, the advice provided is intended to be general. Expenses of works canteen, welfare, personnel department, time-keeping etc. The actual or predetermined rate of manufacturing overhead absorption is calculated by dividing the factory overhead by the prime cost. Incurred other actual overhead costs ii. 970; Before we calculate the optimal quantity to order, lets summarize. This is known as primary distribution of factory overheads. The term material describes a relatively large amount. Understand how manufacturing overhead costs are assigned to jobs. Maintenance of building Area or labour hours. The predetermined overhead rate calculation for Custom Furniture is as follows: \[\begin{split} \text{Predetermined overhead rate} &= \frac{$30\; estimated\; overhead\; costs}{38000\; estimated\; direct\; labor\; hours} \\ \\ &= $30\; \text{per direct labor hour} \end{split}\]. Thus, the absorption rate would be $100,000/200,000 = $0.5. And then allocate the overheads to jobs, products, etc. It gives due consideration to time factor. Sometimes, the basis will be the Ability to pay method, i.e., ability of the department to bear such share of items of overheads. Make the journal entry to close the manufacturing overhead account assuming the balance is immaterial. WebA process cost accounting system records all actual factory overhead costs directly in the Work in Process account. One entry is to transfer the inventory from finished goods inventory to cost of goods sold and is at the cost of the product. 2. The activity used to allocate manufacturing overhead costs to jobs is called an allocation base7 . Furthermore, these costs decrease with an increase in output and increase with a decrease in output. When only one kind of article is produced. { "2.01:_Introduction" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.

Factory Overhead Formula 4. WebAccurate recording and analysis of actual overhead costs are crucial for determining product pricing, budgeting, and financial planning. Managers prefer to know the cost of a job when it is completedand in some cases during productionrather than waiting until the end of the period. As mentioned earlier, the indirect costs do not include direct material and direct labor costs of producing goods and services. As the name suggests, the semi-variable costs are the expenses that are partially fixed and partially variable. Such expenses are, however, not directly related to production, selling, and distribution. For example, wages paid to the salespeople, travel expenses, etc. Terms and conditions, features, support, pricing, and service options subject to change without notice. viii. Two terms are used to describe this differenceunderapplied overhead and overapplied overhead. Accordingly, Overhead costs are classified into indirect material, indirect labor, and indirect overheads. It is easy to understand. AccountingNotes.net. Sales and Marketing Costs: AbbVie spends heavily on marketing and promotional activities to increase brand awareness and drive sales. Content Filtration 6. Dec 12, 2022 OpenStax. (attribution: Copyright Rice University, OpenStax, under CC BY-NC-SA 4.0 license), Creative Commons Attribution-NonCommercial-ShareAlike License, https://openstax.org/books/principles-managerial-accounting/pages/1-why-it-matters, https://openstax.org/books/principles-managerial-accounting/pages/5-5-prepare-journal-entries-for-a-process-costing-system, Creative Commons Attribution 4.0 International License. iii. xi. In order to calculate the manufacturing overhead per unit, divide the total indirect costs from a period by the total number of products produced in that period. WebThe Sweet Shop records applied (estimated) overhead to Job Cost Sheets as a percentage of Direct Labor Costs. How do companies assign manufacturing overhead costs, such as factory rent and factory utilities, to individual jobs? As stated earlier, the overhead rate is calculated using specific measures as the base. Canada Goose Is a 900 winter jacket really worth it. Electric lighting Number of light points or areas. The bill will be paid next month. The OpenStax name, OpenStax logo, OpenStax book covers, OpenStax CNX name, and OpenStax CNX logo ii. Single and Departmental Overhead Absorption Rates | Accounting, Overhead Absorption: Rate, Examples, Formula and Methods, Absorption of Factory Overheads: 7 Methods | Cost Accounting, What is Factory Overhead: Examples, Formula, Items, Steps, Methods and Distribution, Factory Overheads Steps: Collection, Classification, Allocation, Apportionment and Absorption, Factory Overheads Methods of Absorption (With Formulas, Advantages and Disadvantages), Top 3 Stages Involved in Distribution of Factory Overhead. consent of Rice University. Accounting. Because manufacturing overhead costs are difficult to trace to specific jobs, the amount allocated to each job is based on an estimate. Machine shop expenses Machine hours or labour hours. *$180 = $30 per direct labor hour 6 direct labor hours. Web- Standard price per kg. are also assigned to each jetliner. Creative Commons Attribution-NonCommercial-ShareAlike License It needs to be an activity common to each department and influential in driving the cost of manufacturing overhead. Such a process is called absorbing the overheads to various cost units. BACK TO BASICS ESTIMATING SHEET METAL FABRICATION COSTS. ! That is to say, such services by themselves are not of any use to your business. Apart from advertising, overhead costs also include production overheads, administration, selling, and distribution overheads. Most companies simply close the manufacturing overhead account balance to the cost of goods sold account. Estimated or actual time spent. ii. If the costs for direct materials, direct labor, and factory overhead were $522,200, $82,700, and $45,300, respectively, for 16,000 equivalent units of production, the conversion cost per equivalent unit was $8.00. (d) According to number of workers employed. Insurance Machine value considering insurance period. If the products of a manufacturing process are produced to customer specifications, a process cost system is more appropriate than a job order cost system. A manufacturing overhead account is used to track actual overhead costs (debits) and applied overhead (credits). Disclaimer 8. Accordingly, overhead costs on the basis of function are categorized as follows. How do we close the manufacturing overhead account? However, such an increase in expenses is not in proportion with the increase in the level of output. This careful tracking of production costs for each jetliner provides management with important cost information that is used to assess production efficiency and profitability. The journal entry to record the labor costs is: Manufacturing overhead includes indirect material, indirect labor, and other types of manufacturing overhead. A rate established prior to the year in which it is used in allocating manufacturing overhead costs to jobs. These include gas and electricity, depreciation on manufacturing equipment, rent and property taxes on manufacturing facilities, etc. In this method, direct labor cost is taken as a base for absorbing the overhead costs. The estimated annual overhead cost is $340,000 per year. Legal. Overhead Rate = (Overheads/Direct Wages) * 100. 8. There may be three broad categories of factory overheads: 2. Bookkeeping is simplified by using a predetermined overhead rate. Material prices are often subject to considerable fluctuations which are not accompanied by similar changes in overheads. The process of creating this estimate requires the calculation of a predetermined rate. Overheads such as depreciation of buildings, plant and machinery, fire insurance premiums on these assets, etc. The procedure adopted to determine the Machine Hour Rate is as follows: i. The value of the inventory transferred to finished goods in the production cost report is the same as in the journal entry: Each unit is a package of two drumsticks that cost $8.40 to make and sells for $24.99. Depreciation Actual depreciation as per Plant Register. Each financial situation is different, the advice provided is intended to be general. Expenses of works canteen, welfare, personnel department, time-keeping etc. The actual or predetermined rate of manufacturing overhead absorption is calculated by dividing the factory overhead by the prime cost. Incurred other actual overhead costs ii. 970; Before we calculate the optimal quantity to order, lets summarize. This is known as primary distribution of factory overheads. The term material describes a relatively large amount. Understand how manufacturing overhead costs are assigned to jobs. Maintenance of building Area or labour hours. The predetermined overhead rate calculation for Custom Furniture is as follows: \[\begin{split} \text{Predetermined overhead rate} &= \frac{$30\; estimated\; overhead\; costs}{38000\; estimated\; direct\; labor\; hours} \\ \\ &= $30\; \text{per direct labor hour} \end{split}\]. Thus, the absorption rate would be $100,000/200,000 = $0.5. And then allocate the overheads to jobs, products, etc. It gives due consideration to time factor. Sometimes, the basis will be the Ability to pay method, i.e., ability of the department to bear such share of items of overheads. Make the journal entry to close the manufacturing overhead account assuming the balance is immaterial. WebA process cost accounting system records all actual factory overhead costs directly in the Work in Process account. One entry is to transfer the inventory from finished goods inventory to cost of goods sold and is at the cost of the product. 2. The activity used to allocate manufacturing overhead costs to jobs is called an allocation base7 . Furthermore, these costs decrease with an increase in output and increase with a decrease in output. When only one kind of article is produced. { "2.01:_Introduction" : "property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass228_0.

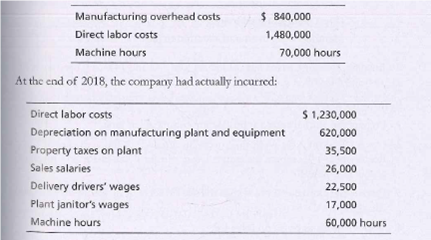

record other actual factory overhead costs